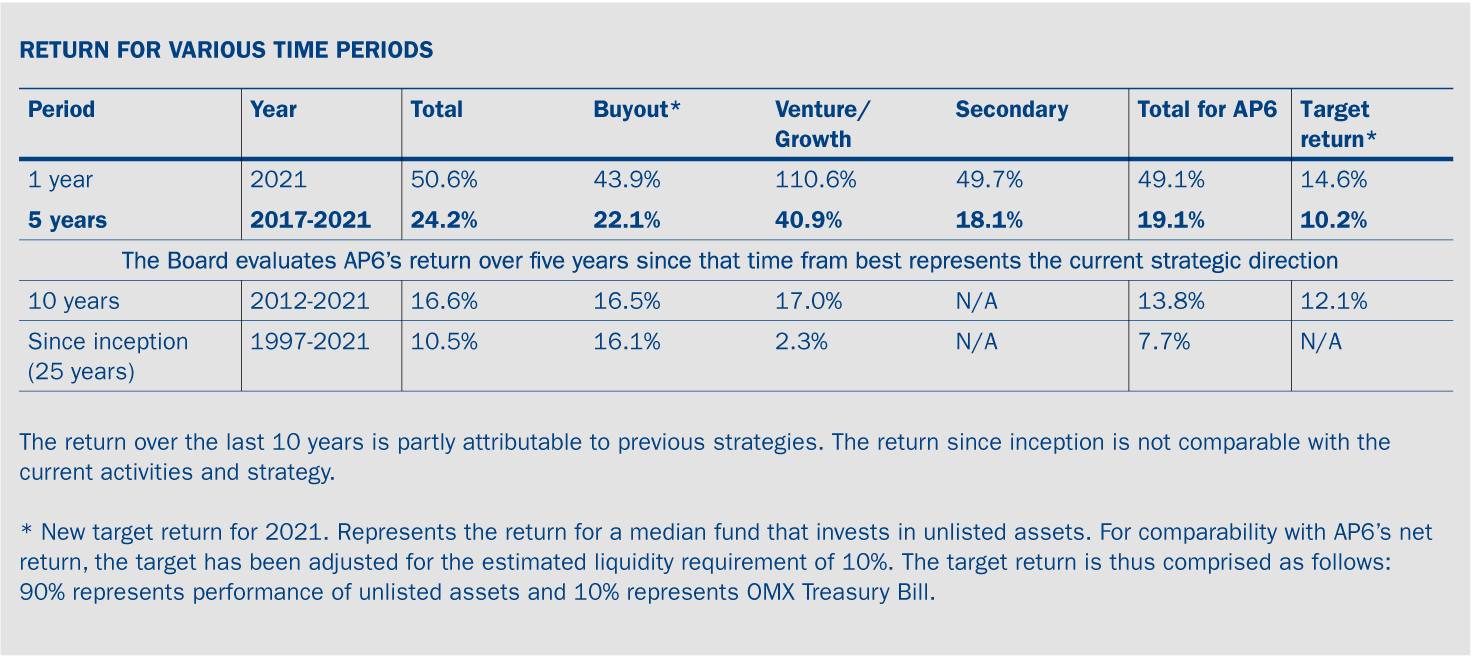

Burgiss benchmark 5 year return + 10% liquidity management (OMX T-Bill)

- As of 2021, AP6 has a new target return based on how a median fund within the unlisted asset class has returned during the past five-year period.

- Unlike a traditional PE fund, AP6 is a closed-end fund, which means that there are no inflows or outflows of capital. A liquidity buffer (10% of fund capital) is thus needed to meet the investment obligations, which can vary over time. The target return for the liquidity reserve is the OMX Treasury Bill.

- The target return is thus comprised as follows: 90% represents performance of unlisted assets and 10% represents OMX Treasury Bill.

- Burgiss who is a leading player in its field, is the provider of unlisted data. The data is based on General Partners’ reporting to their Limited Partners, so the return is calculated net of fees so it can be compared to AP6’s results. It is not specific to a particular geographic area, since AP6 is not limited by such. Because AP6’s earnings are translated to SEK, the return data from Burgiss is also translated to SEK, so that it is comparable.